The global EV battery supply chain has officially entered its “Industrial Maturity” phase. In the first week of March 2026, the narrative shifted from a frantic race for raw minerals to a sophisticated orchestration of domestic resilience and circular economics. For C-suite leaders, the update is clear: the focus is no longer just on securing the supply, but on mastering the data and chemistry that underpin it.

1. The “Buy European” Mandate: The Industrial Accelerator Act (IAA)

On Wednesday, March 4, 2026, the European Commission introduced the Industrial Accelerator Act (IAA). This is Europe’s most aggressive move yet to decouple its green transition from external dependencies.

- The Mandate: Publicly subsidized EVs must now undergo final assembly within the EU, with at least 70% of components (excluding the battery) manufactured locally.

- Strategic Impact: While the 2035 combustion engine ban remains the North Star, the IAA creates a “lead market” for European-made clean tech, forcing global players to localize production or face exclusion from massive government contracts.

2. India’s Giga-Ambition: The Jamnagar Scaling

In parallel, Asia’s energy landscape is being reshaped by India’s rapid industrialization. Reliance Industries confirmed this week that its integrated battery giga-factory in Jamnagar is on track for a late-2026 launch.

- Capacity: The facility will start at 40 GWh per year, with a modular roadmap to scale to 100 GWh.

- The Ecosystem: Unlike traditional standalone plants, this is part of a “Sand-to-Electrons” ecosystem, integrating solar, hydrogen, and battery storage under one roof to drive down the total cost of energy.

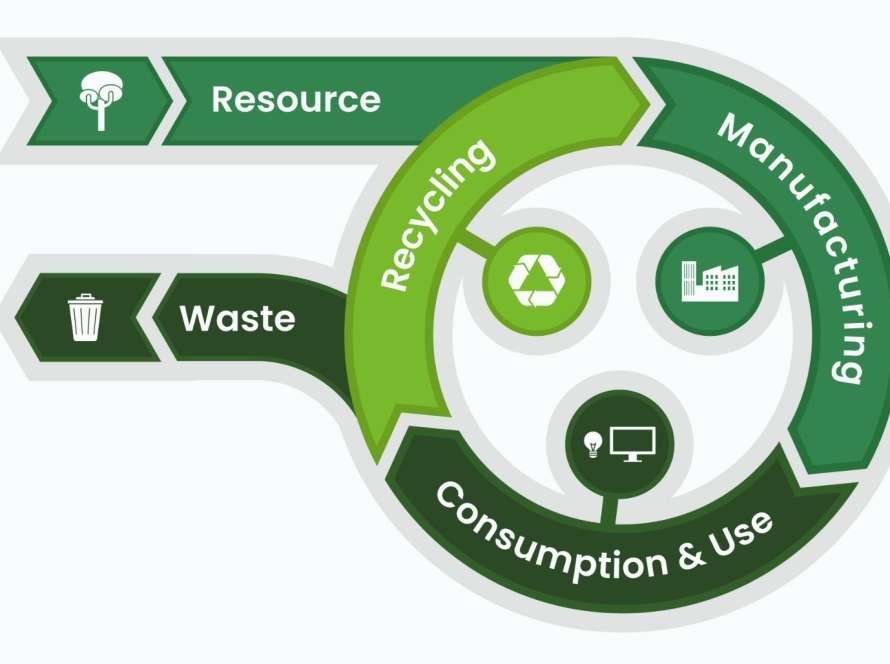

3. The End of “Collect and Bury”: 99% Recovery Benchmarks

A major technological milestone was reported on March 3, 2026, regarding Direct Cathode Recycling.

- The Breakthrough: New hydrometallurgical-direct hybrid processes are now achieving 99.9% recovery of battery-grade lithium, cobalt, and nickel from end-of-life cells.

- The Bottom Line: By 2027, the EU Battery Passport will be mandatory. This week’s progress in direct recycling means that the “circularity premium” is finally shrinking, making recycled minerals nearly cost-competitive with virgin materials for the first time.

4. Next-Gen Chemistry: The 500 Wh/kg Threshold

While Lithium-Iron-Phosphate (LFP) remains the workhorse for mass-market EVs, Solid-State and Sodium-Ion technologies have moved into pilot-scale validation this week.

- High-Density Labs: Multiple firms in East Asia and North America have released 500 Wh/kg high-energy-density samples to OEMs for testing.

- Sodium-Ion Scaling: Sodium-ion batteries are now being positioned as the primary solution for the $25,000 EV segment, significantly reducing the industry’s reliance on high-cost lithium carbonate.

Strategic Hurdles for the C-Suite

As the supply chain matures, executive teams must address three primary complexities:

- Digital Traceability: The upcoming Battery Passport requirements mean that “ESG-blind” sourcing is now a legal liability. Every gram of mineral must have a digital twin from the mine to the dashboard.

- Chemistry Agility: With Sodium-ion and Solid-state reaching maturity, your 2030 fleet strategy must be “chemistry agnostic” to avoid getting locked into stranded battery architectures.

- The Talent Gap: The shift from mechanical assembly to electrochemical simulation requires a new breed of workforce. Managing a Giga-factory in 2026 is a software-first enterprise.

The Bottom Line

The EV battery supply chain is no longer a wild frontier of resource grabbing; it is a precision-engineered network defined by transparency and chemistry innovation. Whether you are navigating the new EU assembly mandates or the scaling of LFP recycling, the winners of 2026 are those who view their batteries as “renewable mineral banks” rather than disposable fuel tanks.